Investing is all about finding the most appropriate balance of risk and return, not just for an asset but also at the portfolio level. Risk is hard to quantify but, broadly, the longer the timeframe over which someone invests, the more risk they are able to accept and the more likely their investment is to do well.

The Barclays Equity Gilt Study has been published every year since 1956 using UK data dating from 1899 and US data going back to 1925. What it shows, unequivocally, is that equities – shares – significantly outperform UK Government bonds (Gilts) US Government Treasury Bills (T-Bills), and cash over the long term. The losses we saw across major asset classes in 2022 thanks to Putin’s invasion of Ukraine, combined with a sharp rise in policy rates in the last year, have meant that cash has become investable again in the eyes of many. After a decade of negligible interest rates, those now available on savings accounts look comparatively attractive.

While savings account rates are higher today than they have been for over a decade, they are still significantly lower than inflation. By holding cash, you are guaranteeing a real loss of purchasing power.

We have seen some torrid returns in the last few quarters, so it is understandable that investors are cautious. Holding cash when financial markets are falling is obviously a good strategy. By holding cash though, you are not only ensuring you do not participate in any downturn, but you are also ensuring you will not participate in any upturn. Now think back to the Barclays study. When equities have a solid long-term track record of beating cash deposits, holding cash instead of shares pretty much guarantees that you’ll be worse off in the long term.

Timing markets is hard and the most rewarding days to be invested often occur as a new dawn is breaking following a market downturn. Those invested in cash are likely to miss out on these days, particularly if they have tied their money into fixed-term cash products. Buying opportunities are often only obvious in hindsight.

Although cash can provide a monthly interest payment, several asset classes are also able to provide attractive income rates at the moment. The Vanguard UK Equity Income Index fund, for example, is currently on a historic yield of circa 5%. Law debenture, an Investment Trust founded in 1899 which I’ve been personally buying for myself and clients since 1985 is yielding around 4%, has a superb record of growing dividends year on year, and has increased its share price by around 60% in the last ten years in addition to the income it’s generated. You get the general idea.

Market volatility can be hard to stomach but the ups and downs of the markets are the price of entry. Over the long term, investment strategies with this in mind can produce outsized returns, while cash deposits will not.

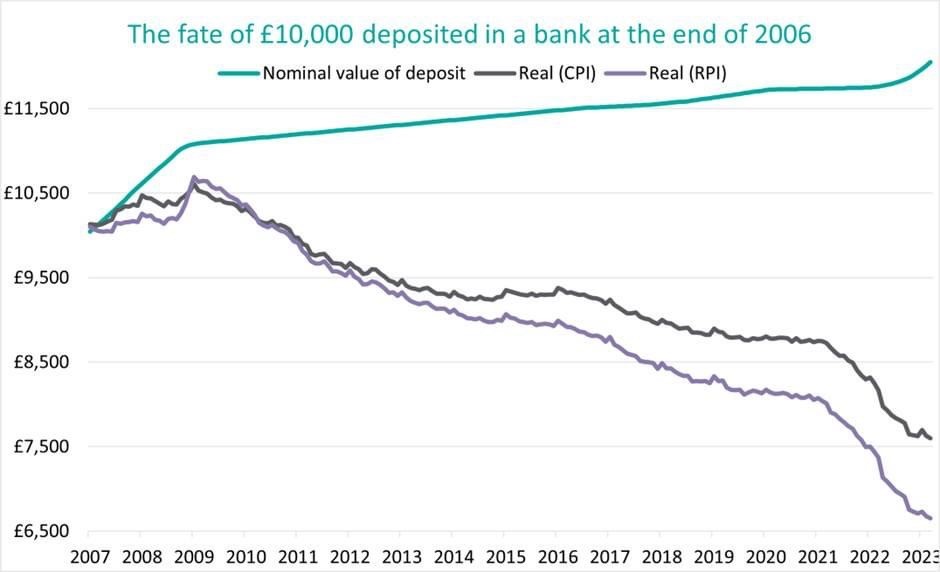

The chart below shows the decline in the buying power of cash held on deposit. The green line is what you see when you look at your building society deposit book, a balance steadily increasing with interest added. The other lines are the real picture once inflation is taken into account, RPI and CPI.

Where’s our money, mine and my wife’s and our kids? In the market. In shares. We put our money where our mouth is.

Chart: Source: Bloomberg, Waverton 31.03.2023